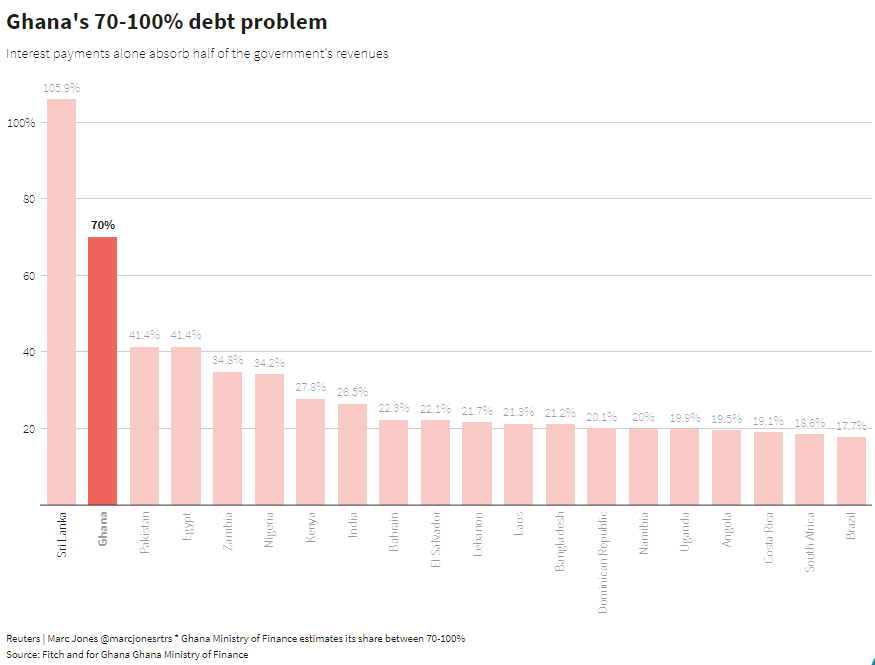

Ghana’s public debt amounts to more than 100 per cent of its gross domestic product, and payments to service this debt regularly range between 70% and 100% of government revenue. The country’s debt stock as of November 2022 was GHS575.7 billion, the Bank of Ghana revealed.

As a result of this, both the president, Nana Akufo-Addo and his Finance Minister, Ken Ofori-Atta, have admitted the country is in a dire financial crisis. Government has, therefore, turned to the International Monetary Fund (IMF), albeit reluctantly, for a solution to the crisis. But the steps towards a complete IMF intervention have become a careful walk through an economic landmine.

DUBAWA, therefore, explores Ghana’s current economic crisis and its debt exchange programme (DEP), what contributed to the country’s present economic state, the government’s plans out of the doldrums, and the murky parliamentary drama over whether the programme had already received parliamentary scrutiny and approval.

Debt to GDP

The government has been clear towards the end of 2022 that the sustainability of the country’s debt, currently estimated by the World Bank to be at 105% of GDP, has continuously been affected by the negative impact of exchange rate depreciation, particularly on external debt, as well as the crystallisation of significant contingent liabilities. You can find this on page 35 of the World Bank Group report titled ‘Food System Opportunities in a turbulent time.’

In a statement published on the website of the Ministry of Finance and Economic Planning dated December 19, 2022, the government blamed the downturns caused by the COVID-19 pandemic and the Russian-Ukraine war for Ghana’s major economic and financial crisis.

As part of efforts to restore macroeconomic stability and save the economy from collapse, the government has requested a US$3 billion bailout from the IMF.

The yet-to-be-approved three-year IMF assistance is contingent upon Ghana restructuring its public debt – domestic and external. This means that persons and/or institutions that lent money to the government by purchasing bonds would have to agree to defer the repayment period.

Ghana’s debt restructuring program will be in two forms – the Domestic Debt Exchange Programme (DDEP) and the External Debt Restructuring Programme, the Finance Minister, Ken Ofori-Atta, noted in his presentation to Parliament on February 16, 2023. Please refer to paragraphs 31 and 43 of the Finance Minister’s statement to the lawmakers.

What is the Domestic Debt Exchange Programme about?

As its name suggests, the Domestic Debt Exchange Programme is a public offer to Ghanaian bondholders to trade their high-yielding bonds for lower-yielding versions of much longer maturity periods. The eligible bondholders of domestic notes and bonds of the Republic, E.S.L.A Plc and Daakye Trust Plc will have to exchange approximately GHS 137.3 billion (US$11.5 billion or about 15% of 2021 GDP) for a package of 12 new bonds (initially four), the interest of which will not accrue until 2024, starting at 5% rate in that year and moving up to 10% in 2025.

The Domestic Debt Restructuring Programme was launched in Accra on December 5, 2022, by the Minister of Finance. Mr Ken Ofori-Atta maintained participation in the programme “has always been voluntary,” as outlined in the Exchange Memorandum.

Treasury Bills are completely exempted under the Programme, and the government has assured Ghanaians that “all holders will be paid the full value of their investments on maturity.” The government has extended the deadline for the Domestic Debt Exchange Programme more than three times since January 31, 2023, due to opposition from domestic creditors, who are mostly Ghanaian retirees.

Opposition to the Domestic Debt Exchange Programme

Implementation of the Domestic Debt Exchange Programme had not been smooth sailing. There had been opposition from a section of Ghanaians fronted by two visible groups, the Ghana Individual Bondholders Forum and the Pension Bondholders Forum, who had voiced their discontent with the Programme.

The Ghana Individual Bondholders Forum had particularly said its members risked losing about 88.2% of their investments at the current inflation rate under the Programme. Similarly, the Forum maintained that bondholders would lose 71% of their investments when discounted at current Treasury Bill rates and 50% when the coupon rates face a ‘haircut.’

Following a string of picketing at the premises of the Ministry of Finance and Economic Planning by the Pension Bondholders Forum, the government has announced that Pension Bondholders who did not participate in the bond offering are exempted under the Programme. You can find this in paragraph 42 of the statement made by the Finance Minister, Ken Ofori-Atta, to Parliament on February 16, 2023.

Positive subscription rate

Despite the opposition and mass protests spawned by the government’s Domestic Debt Exchange Programme, out of the total GHS97,749,624,691 bonds eligible for tendering, the Ministry of Finance had announced that GHS82,994,510,128 was successfully tendered.

This feat, the government had noted, accounted for about 85% of outstanding eligible amounts, thereby meeting its target of 80% as per the Memorandum of Exchange. Please refer to paragraph 28 of the statement presented to Parliament on February 16, 2023, by the Finance Minister, Ken Ofori-Atta.

Notwithstanding, the government had said that “the GHS 82,994,510,128 bonds that were successfully tendered represents 64% of the outstanding debt stock of GHS 130 billion at the end of December 2022.” Refer to paragraph 29 of the statement presented by the Finance Minister, Ken Ofori-Atta, to Parliament on February 16, 2023.

Does the Domestic Debt Exchange Programme require Parliamentary approval?

While it remained optimistic about the prospects of the domestic market as a major source of funds for its activities in 2023, the government had said some reforms would be needed to achieve this end. This can be found in paragraph 269, page 69 of the 2023 budget presented to Parliament on November 24, 2022.

The government proposed to “undertake reforms including addressing the fragmentation of domestic instruments by consolidating existing bonds to build benchmark bonds, thereby facilitating trading on the secondary market.” Refer to paragraph 269, page 69 of the 2023 budget presented to Parliament on November 24, 2022. Parliament approved the budget on Tuesday, December 6, 2022, despite fierce opposition by lawmakers from the National Democratic Congress (NDC).

Towards the end of the debate on the 2023 Budget, former Minority leader, Haruna Iddrisu, had asked the government to consider cutting down its expenditure to be able to deal with the challenges confronting the economy. He made this appeal minutes before the House approved the controversial Budget.

By approving the 2023 budget christened “Nkabom Budget,” literary translated as ‘Unity Budget,’ Parliament had given its blessing to the government’s policy propositions contained in the document, including the Debt Restructuring Programme, Deputy Majority leader Alexander Afenyo-Markin has said. You can find the clip between minutes 35:25 to 37:21 of the recording of the Parliamentary session uploaded on YouTube by a private media organisation, Joy News.

In a sharp rebuttal, the new Minority leader, Casiel Ato Forson, had noted that Parliament had not approved the government’s Debt Restructuring Programme as asserted by the Deputy Majority leader. Refer to the clip between minutes 41:46 to 43:40 of the YouTube recording of the Parliamentary session.

Data available on YouTube shows that over 1,385 people had viewed the video as of February 19, 2023.

The Member of Parliament for Bolgatanga Central constituency, Isaac Adongo, has backed Mr Ato Forson, saying the “restructuring of the debt of this country is too big for one person to do without taking the input of the people into consideration, and that is why we want it brought to Parliament for approval.” The legislator made the comments hours after the minority in Parliament filed a private members’ motion for the government’s Debt Restructuring Programme to be submitted before lawmakers for deliberation and subsequent approval.

“The President even knows that he doesn’t have the power to take some decisions without the approval of Parliament. The mandate of the people resides in Parliament, and the President and the Finance Minister need to come to Parliament to seek approval because, without that, it has long-standing implications on the sovereignty of Ghana,” he told Accra-based Citi FM.

The stance of the opposition lawmakers has been supported by a leading member of the governing New Patriotic Party (NPP) and a former Attorney-General. According to Mr Ayikoi Otoo, the Debt Restructuring Programme has an international dimension to it because it entails both domestic and external debt restructuring and for that reason, the government requires the approval of Parliament.

“For international commercial transactions, it is important that you come to Parliament for approval,” the private legal practitioner told Accra-based TV3 on February 16, 2023. You can see the video posted on Twitter by TV3 from minutes 4:58 to 7:43.

How international is the Debt Restructuring Programme?

The government’s Debt Restructuring Programme targets both domestic and external creditors. Following the success of the Domestic Debt Restructuring Programme, the government has hinted at plans to engage its partners on the external restructuring programme. “As part of this process, Ghana has officially asked its bilateral creditors for a Debt Treatment initiative under the G-20 Common framework,” the Finance Minister, Ken Ofori-Atta, had said. Refer to paragraphs 43 and 44 of the statement presented by the Finance Minister, Ken Ofori-Atta, to Parliament on February 16, 2023.

“We have started the process of negotiating in good faith with our commercial creditors. Two preliminary discussions and exchange of information have started on a good footing with representative committees and advisors. The members have indicated their commitment to establishing a Creditor Committee to assess Ghana’s request for debt treatment under the Common Framework by the end of February 2023,” the Finance Minister told Ghanaian lawmakers. You can find this in paragraphs 45 to 46 of the statement presented by the Finance Minister, Ken Ofori-Atta, to Parliament on February 16, 2023.

The 1992 Constitution of Ghana in Article 181(1) provides that “Parliament may, by a resolution supported by the votes of a majority of all the Members of Parliament, authorize the Government to agree with the granting of a loan out of any public fund or public account.”

Clause (2) of the said article says the agreement mentioned in clause (1) “shall be laid before Parliament and shall not come into operation unless a resolution of Parliament approves it.”

Also, Article 181(3) of the 1992 Constitution is clear that “No loan shall be raised by the Government on behalf of itself or any other public institution or authority otherwise than by or under the authority of an Act of Parliament.”

What constitutes a “loan” has been defined in clause (6) of Article 181 of the 1992 Constitution to include “any money lent or given to or by the Government on condition of return or repayment, and any other form of borrowing or lending in respect of which;

(a) money from the Consolidated Fund or any other public fund may be used for payment or repayment; or (b) money from any fund by whatever name, established for payment or repayment, whether directly or indirectly, may be used for payment or repayment.”

There is a long line of judicial pronouncements on what constitutes an “international transaction” in Ghana. These decisions include Attorney-General v Faroe Atlantic Co Ltd, Dr Mark Assibey-Yeboah v Electricity Company of Ghana, and Attorney-General v Balkan Energy, among others.

The Supreme Court in [Attorney-General v Balkan Energy] had held that: “a business transaction is “international” within the context of Article 181 (5) where the nature of the business, which is the subject-matter of the transaction is international in the sense of having a significant foreign element or the parties to the transaction (other than the Government) have a foreign nationality reside in different countries or, in the case of companies, the place of their central management and control is outside Ghana.” Please refer to page 3 of the decision here.

In an attempt to expand the scope of “international transaction,” the apex court held in [Attorney-General v Balkan Energy] that “Given the complexity of contemporary international business or economic transactions, there will be transactions of such a clear international nature that they should come within any reasonable definition of an international business or economic transaction, but which may have been concluded with the Ghana government by an entity resident in Ghana. In such a situation, we believe that the substance, rather than the form, should prevail. What we have just said begs the question of what “international” means. In this connection, we think that there is a need to combine both the nature of the business or economic transaction criterion and the parties criterion proposed by the plaintiff in his submission to formulate a test for determining what transactions come within the ambit of article 181 (5) of the 1992 Constitution”

However, the Supreme Court was emphatic in [Dr Mark Assibey-Yeboah v Electricity Company of Ghana, Ghana National Petroleum Authority and the Attorney-General] that international transactions by statutory corporations with commercial functions could not be said to be transactions conducted by the government and therefore require no prior Parliamentary approval as prescribed in article 181(5) of the 1992 Constitution. Holding otherwise, the court had noted, “would probably increase the weight of Parliament’s responsibilities in this regard to an unsustainable level. Accordingly, it is reasonable to infer that the framers of the 1992 Constitution did not intend such a result.” You can find this on page 22 of the judgment.

Conclusion

It is not yet clear what the outcome of the private members’ motion filed by the minority on the government’s Debt Restructuring Programme would be.

However, what is clear is that the Ghanaian Government is racing against time to secure the US$3 billion Extended Credit Facility from the International Monetary Fund. Ghana’s commitment to its public debt restructuring will be crucial to securing the overwhelming approval of the Fund’s Executive Board.